How Employers Can Reduce Soaring Healthcare Costs Due to Chronic Conditions

Learn how prevention, wellness, and disease management can improve employee health and reign in absenteeism and long-term healthcare costs.

The IRS has announced the 2018 contribution limits for FSA and HSA participants. For individuals, the 2018 maximum contribution amount is ...

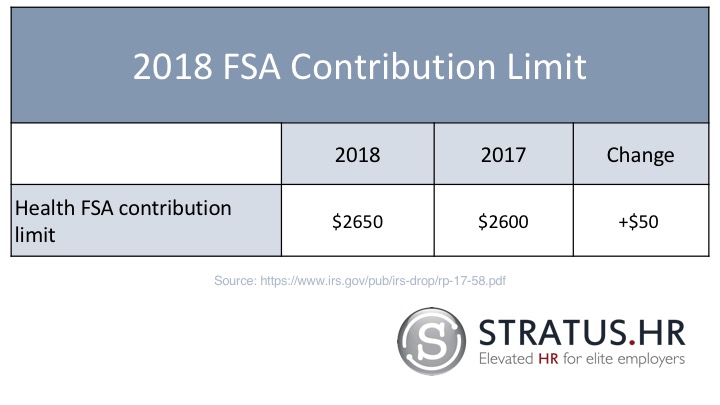

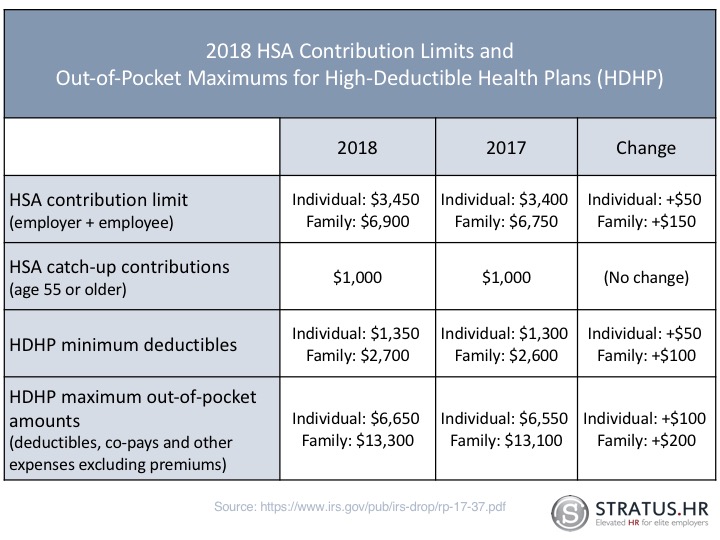

The IRS has announced the 2018 contribution limits for health flexible spending accounts (FSA), as well as limits for health savings accounts (HSA) for those with a qualifying high deductible health plan (HDHP). For 2018, FSA contribution limits will cap at $2,650 (an increase of $50 from 2017), and HSA limits will be at $3,450 for self or $6,900 for family (click on the side charts for more details).

Flexible spending allows participants to set aside pre-tax dollars to apply to the upcoming calendar year’s out-of-pocket expenses related to eligible medical, dental, vision, pharmacy and dependent care. The major advantage to enrolling in FSA is lowering your taxable income.

Per IRS guidelines, up to $500 of any unused dollars left in your FSA account at the end of the year can be rolled over and used in the subsequent year for eligible expenses. The rollover amount does not count towards the annual election limit of $2,650. Any unused amount in excess of $500 will be forfeited.

Open enrollment is the only time, barring qualified life events, when eligible employees can enroll in FSA benefits for the upcoming calendar year. Flex spending dollars can be used in addition to other insurance plans. Open enrollment has an effective date of January 1, 2018. Please watch for more details about FSA open enrollment for 2018.

If you are currently participating in a Qualified High Deductible Health Plan (HDHP), you are eligible to contribute pre-tax dollars to an HSA. An HSA is similar to an FSA, in that they both lower your taxable income and are used to pay for eligible health care expenses. The HSA differs from the FSA in that it has a higher maximum annual contribution ($3,450), and the money in your account accrues from year to year like a bank account and earns interest. In other words, if you don't use it, you don't lose it. You can also change your HSA contribution throughout the calendar year.

If you do not currently participate in an HDHP, you will not be eligible for an HSA. If you participate in an HSA, you cannot participate in an FSA, too. (Exception: you may have a limited-purpose FSA, which can be used for dental and vision expenses only, not medical expenses.)

For more information about FSAs, HSAs, open enrollment, or any other benefit-related question, please contact our benefits team at benefits@stratus.hr.

Learn how prevention, wellness, and disease management can improve employee health and reign in absenteeism and long-term healthcare costs.

Learn how month-in-advance premiums ensure uninterrupted coverage, as well as what employees should expect for catch-up deductions and long-term...

When employees qualify for FMLA but need to take time off in smaller blocks of time, it's called intermittent leave. Here’s how it works.