Working remotely? Tips for success

Whether you are new to telecommuting or have been working remotely for years, here are 8 tips for success while working away from the office.

The CARES Act provides small businesses more immediate help to keep workers employed and business expenses covered while enduring setbacks due to COVID-19.

*Please note: subsequent COVID-relief legislation has made some of the content in this article no longer applicable.

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) was signed into law on March 27, 2020, and is intended to help keep employees paid and employer debt obligations funded, despite business setbacks from the Coronavirus. Here’s what you need to know.

Companies with fewer than 500 employees and other businesses can apply for an emergency SBA-guaranteed loan that may be 100% forgiven when the loan amount is used to maintain payroll for 8 weeks, beginning with when they receive their loan. Costs for payroll, mortgage interest, rent payments, and utility payments (for properties that existed prior to Feb 15, 2020) during those 8 weeks may all be forgiven.

These loans require no personal guarantee or collateral. There are no application fees or closing costs, and the availability of credit from other sources will not disqualify eligibility. As the intent is to keep workers employed and paid, anyone that may have been laid off due to COVID-19 can be rehired and paid with wages through this program.

The formula for calculating your PPP max loan amount is:

(Average monthly payroll costs) X 2.5 = total loan amount (capped at $10 million)

To find your average monthly payroll costs, look at your total monthly payments during the 1-year period prior to the date your loan is made and find the average. If you were not in business in 2019, look at your average monthly payroll between January and February, 2020

Monthly payments are deferred for 6 months with a modest interest rate of 1% and a maturity of 2 years. (UPDATED: April 3, 2020)

Companies may also qualify for an Economic Injury Disaster Loan as long as the two loans don’t pay for the same expenses. Check with your lender for more information.

Eligible businesses may also be eligible for:

Talk with your tax professional to know which apply to your business.

Please note: this summary is not all-inclusive. For a more thorough summary, please see the Coronavirus Emergency Loans Small Business Guide and Checklist provided by the U.S. Chamber of Commerce or NAPEO's summary of payroll assistance programs.

The CARES Act may help you pay for 8 weeks of employee wages and business expenses.

Sources:

Treasury.gov

US Chamber

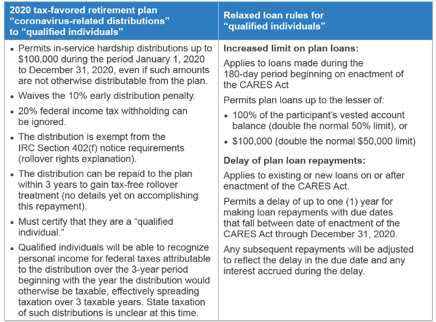

Here's a list of key provisions to the CARES Act that impact qualified retirement plans.

Related articles:

Whether you are new to telecommuting or have been working remotely for years, here are 8 tips for success while working away from the office.

Discover how your company compares with others through employee benefits benchmarking. Learn about the key indicators and effective strategies here.

Regardless of whether you were pro or against OSHA's vaccine mandate, SCOTUS ruled OSHA has no authority to authorize such a measure.