Working remotely? Tips for success

Whether you are new to telecommuting or have been working remotely for years, here are 8 tips for success while working away from the office.

As companies wade through updated guidance of the PPP loan, we've outlined our list of employer-asked FAQs to help them dissect the regs.

The SBA Paycheck Protection Program (PPP) seems to be the most attractive option for small businesses experiencing hardship created by the Coronavirus. Due to the rushed legislation, there has been a lot of follow-up clarification to provide more specific guidance.

Read our list of FAQs regarding PPP loan forgiveness.

No, page 6 of the Interim Final Rule (IFR) does not specify requiring Form 941. It states:

“You must… submit such documentation as is necessary to establish eligibility such as payroll processor records, payroll tax filings, or Form 1099- MISC, or income and expenses from a sole proprietorship. For borrowers that do not have any such documentation, the borrower must provide other supporting documentation, such as bank records, sufficient to demonstrate the qualifying payroll amount.”

The PPP Application language has also been revised to omit anything about a Form 941 requirement.

Applicants must submit SBA Form 2483, along with proper documentation. The IFR specifies “such documentation as is necessary to establish eligibility such as payroll processor records, payroll tax filings[...]. For borrowers that do not have any such documentation, the borrower must provide other supporting documentation, such as bank records, sufficient to demonstrate the qualifying payroll amount.”

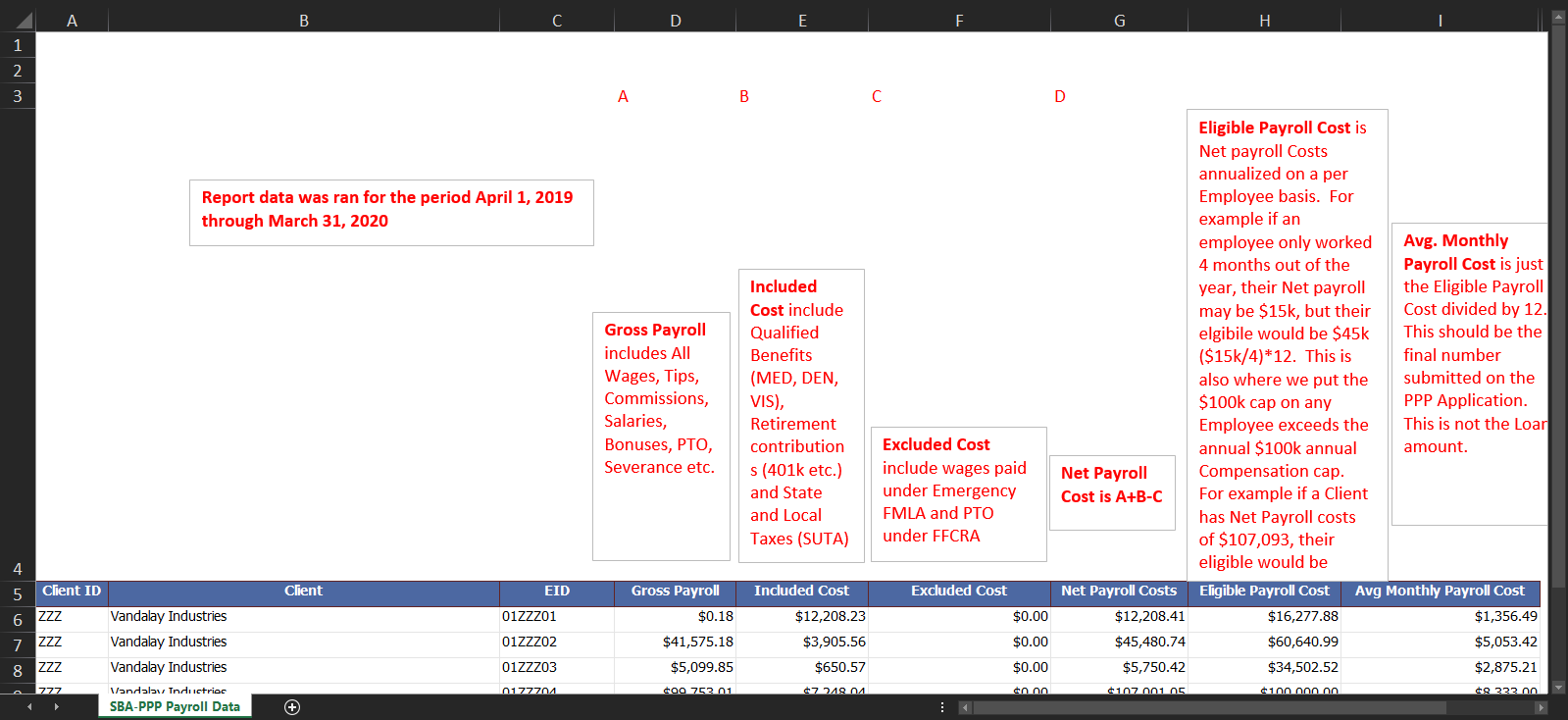

Stratus.hr clients already have this information but may need to portray it in a way their lender requests. The below image explains the data encompassed in each section of the spreadsheet sent to clients. All other lender-requested information can be found in the user dashboards of the Stratus.hr System.

Pages 11 and 15 of the IFR state: "No, independent contractors have the ability to apply for the PPP loan on their own so they do not count for purposes of a borrower's PPP loan calculation… [or] a borrower’s PPP loan forgiveness."

Page 10 of the IFR specifies payroll costs as compensation to employees who live in the US that include:

There is no specific clarity on this. At this point, it appears unlikely either of these will be forgivable.

While this has changed several times since the legislation was first released, page 11 of the IFR states the final interest rate is 1% with a maturity of 2 years.

The loan amount is determined entirely off of an estimated monthly payroll cost (average monthly payroll costs X 2.5). The forgiveness component takes into account the actual 8-week period from loan origination and includes payroll costs, rent, utilities, etc. Page 14 of the IFR specifies that not more than 25% of the loan forgiveness amount may be used for nonpayroll costs if you’re seeking 100% forgiveness, as the core purpose of the loan is to keep employees paid and insured. In other words, if you have an expensive rent lease, you may not have that amount entirely forgiven if it exceeds more than 25% of the loan amount.

No, page 15 of the IFR specifies the proceeds of a PPP loan are to be used for “i. payroll costs (as defined in the Act and in 2.f.); ii. costs related to the continuation of group health care benefits during periods of paid sick, medical, or family leave, and insurance premiums…” Remember that the purpose of this emergency loan is to keep employees paid and insured.

The SBA seems to make a flat $100k cap for everything, including benefits, but more clarification is needed in this regard.

The statute doesn’t really account for employees that quit; it is strictly based on employee headcount. Consider hiring a replacement to maintain your headcount, as the forgiven amount will be reduced if your headcount decreases.

Yes, this is written into the statute to account for this. You can cure any previous reduction in staff if you do so by June 30, 2020 to qualify for full loan forgiveness.

Yes! If your business needs the added help, don't wait to apply!

We anticipate further guidance to be issued regarding loan forgiveness and will provide more details as we receive them. If you have questions about this loan, please contact your certified HR expert.

Have more questions about the PPP loan? Contact your certified HR expert.

Whether you are new to telecommuting or have been working remotely for years, here are 8 tips for success while working away from the office.

Discover how your company compares with others through employee benefits benchmarking. Learn about the key indicators and effective strategies here.

Regardless of whether you were pro or against OSHA's vaccine mandate, SCOTUS ruled OSHA has no authority to authorize such a measure.